Life insurance is an important part of planning for the future especially for people with families who want to make sure they are protected and have money when they need it. There are kinds of insurance policies but one that stands out is adjustable life insurance. This type of insurance is special because it lets people make changes as their needs change over time.

A lot of people go through changes in life like getting married having kids getting a new job or retiring. These changes can affect how insurance they need. That is why adjustable life insurance is becoming more popular. It is one reason why people like it because it lets them make changes as their needs change.

Adjustable life insurance can also be a little tricky. Before buying a policy it is very important to understand how it works what is good about it. What is not so good. Some people really like it. Others might like simpler insurance options better.

In this guide we will talk about the features of adjustable life insurance, its benefits and risks and how it compares to whole life insurance. We will also explain how cash value works in the policy.

What Is Adjustable Life Insurance?

Adjustable life insurance is a type of life insurance that lets people make changes to their policy over time. They can change how much they pay, how much their family gets if they die or how long they are covered.

Unlike whole life insurance, which usually has fixed payments and benefits adjustable life insurance is flexible. If someone gets a raise they can pay more to increase their benefits. If they are having a time they can pay less for a while.

This flexibility makes life insurance attractive to people who think their financial situation will change over time. The policy also has a cash value component that grows over time. Part of each payment goes into an account that earns interest and grows.

Because adjustable life insurance combines protection with features many people think it is a great tool for planning for the future.

How Adjustable Life Insurance Works

To decide if adjustable life insurance is right for you you need to understand how it works. The policy starts with a base payment and benefit amount that you choose. Over time you can make changes based on your needs and the insurance company rules.

For example a young parent might start with coverage to protect their kids. Later when the kids are grown they can reduce coverage and lower payments. If they get a raise they can pay more to grow their cash value

The cash value grows with interest. Some policies guarantee a growth rate while others depend on how well the market does.

This ability to make changes over time is one reason people choose life insurance over other types of insurance.

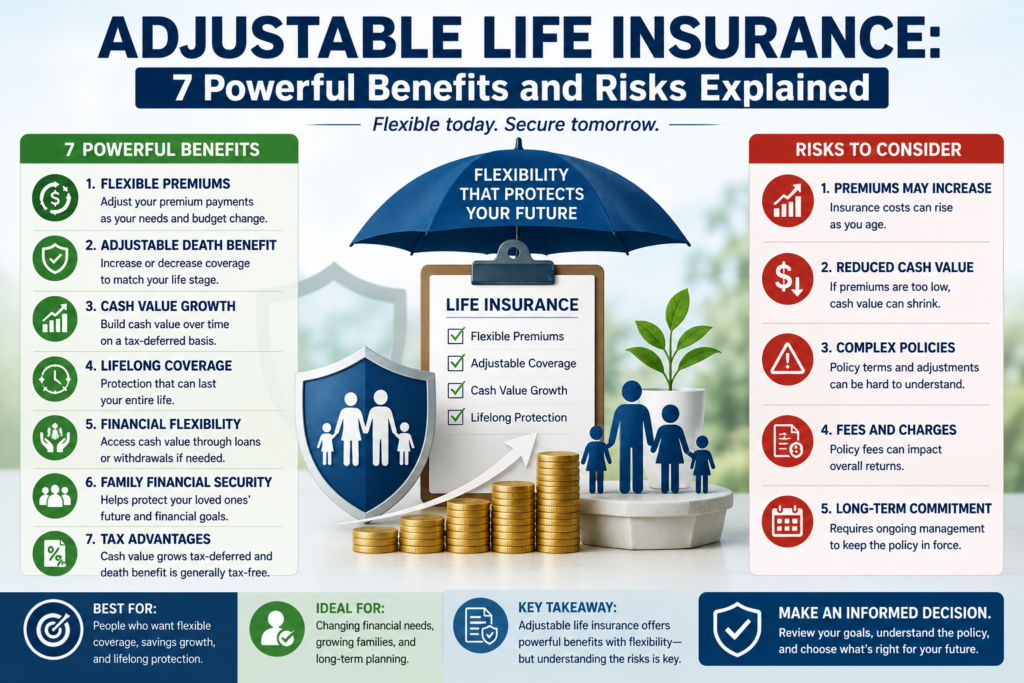

Benefit #1: Flexible Payments

One of the things about adjustable life insurance is that you can change your payments. Traditional life insurance policies usually require fixed payments that stay the same over time.. Adjustable policies let you make changes within certain limits.

If you are having a time you can lower your payments or use your cash value to help. This can reduce stress during hard times. On the hand if you get a raise you can pay more to grow your cash value faster.

Because life is unpredictable flexible payments are very valuable. Many families like this feature because it lets them keep their insurance when things are uncertain.

Benefit #2: Adjustable Benefits

Another big advantage of adjustable life insurance is that you can change your benefits. Life insurance needs are not always the same. Your financial responsibilities might increase after you get married have kids buy a house or start a business.

Adjustable policies let you increase coverage when you need protection. Later when your debts decrease and your dependents are grown you can reduce coverage. This can help you avoid paying much for insurance you do not need.

In some cases increasing your benefits might require a check-up.. Reducing coverage is usually simpler.

Being able to customize your benefits makes adjustable life insurance very adaptable to stages of life.

Benefit #3: Cash Value Growth

One of the advantages of adjustable life insurance is that it can build cash value over time. Unlike term life insurance, which only provides death benefits adjustable life insurance includes a savings component that grows gradually as you pay premiums.

Whenever you pay a premium part of the money goes toward maintaining your insurance coverage. Another part is added to your cash value account. Over time this account grows based on interest rates or policy performance.

The growth of your cash value is usually tax-free. This means you do not pay taxes on the earnings long as the money stays in the policy. This tax advantage makes adjustable life insurance attractive, for long-term planning.

You can also borrow money against your cash value if you need it. Many people use these funds for emergencies, education, home repairs, retirement income or business investments.

For example if you have built cash value over the years you can take a policy loan instead of applying for a bank loan. Policy loans often have restrictions and may offer more flexibility.

However borrowing against your cash value can reduce your death benefits if you do not repay the loan. Interest may also apply to loans.

Compared to term insurance adjustable life insurance offers financial value because it combines lifelong coverage with long-term savings growth. Although cash value growth may seem slow at first it can become a financial resource later in life.

This combination of insurance protection and financial accumulation is one reason why many people choose life insurance as part of their overall financial strategy. Adjustable life insurance is a type of life insurance that people like because it is flexible and can be adjusted over time. People can change their life insurance policy to fit their changing needs. Adjustable life insurance has benefits, including flexible payments and adjustable benefits. It also has a cash value component that grows over time which’s a big advantage of adjustable life insurance.

Benefit #4: Lifelong Coverage Explained

One of the things about adjustable life insurance is that it covers you for your whole life.

Unlike term life insurance, which only protects you for a years adjustable life insurance stays active for your entire life if you pay premiums and meet policy conditions.

This means your family will get a death benefit no matter when you pass away.

With term insurance coverage might end before you die especially if you outlive the policy term.

In that case your family may not get any help unless you renew or replace the policy.

Having coverage gives you peace of mind because your family will have financial protection in the future.

This security can help your loved ones pay for funeral expenses, debts, mortgage payments, education costs or daily living expenses after you’re gone.

Another important reason people like coverage is that health conditions can change over time.

As you get older buying an insurance policy might become very expensive or even impossible because of medical issues.

Adjustable life insurance removes this risk because the coverage stays active for life.

Permanent protection is also useful for planning your estate and business succession.

Some families use adjustable life insurance to transfer wealth to generations or to provide financial stability for family businesses after the owners death.

For parents with dependents or individuals wanting guaranteed family support adjustable life insurance creates term financial confidence.

Knowing that your loved ones will get protection regardless of your age or future health conditions is one of the biggest reasons people choose permanent insurance coverage.

Risk #1: Higher Costs

One big downside of adjustable life insurance is that it costs more.

Permanent insurance policies are usually more expensive than term life insurance because they provide coverage and build cash value over time.

The flexibility of policies might also increase administrative costs.

Higher premiums can put pressure on individuals with limited budgets.

While the policy offers long-term benefits some people might find the costs hard to maintain consistently over decades.

Before buying life insurance it’s essential to evaluate long-term affordability carefully.

People who mainly need temporary coverage might prefer term insurance instead.

Risk #2: Policy Complexity

Another significant risk is policy complexity.

Many consumers struggle to understand how adjustable life insurance works because of its flexible structure and cash value features.

Premium adjustments, interest calculations surrender charges and policy fees can become confusing.

Without understanding policyholders might make decisions that negatively affect the policy long-term performance.

For example reducing premiums much could lower cash value growth or even risk policy lapse.

Complex insurance products often require monitoring and professional financial advice.

People who prefer simplicity might find adjustable policies overwhelming.

Risk #3: Investment Uncertainty

Although cash value growth is a benefit it might also involve uncertainty depending on the policy structure.

Some forms of adjustable life insurance might tie returns partly to market performance or interest rates.

If returns are lower than expected the policy might accumulate cash value slowly.

Lower growth could require future premiums to maintain coverage.

This uncertainty makes adjustable life insurance less predictable than whole life insurance with guaranteed returns.

Policyholders should carefully review growth assumptions and guarantees before purchasing coverage.

Understanding the relationship between premiums, interest rates and cash value is extremely important.

Whole Life vs Adjustable Life Insurance

When comparing life vs adjustable insurance the biggest difference is flexibility.

Whole life insurance typically offers premiums, guaranteed death benefits and stable cash value growth.

Adjustable life insurance however allows policyholders to modify premiums and death benefits over time.

Whole life insurance is usually easier to understand and manage because of its structure.

Adjustable policies provide customization but might require more active management.

People who value simplicity often choose life insurance while those wanting financial flexibility might prefer adjustable life insurance.

Both policies provide coverage and cash value accumulation.

The better choice depends on financial goals, income stability and comfort with policy management.

Who Should Consider Adjustable Life Insurance?

Adjustable life insurance might be suitable for individuals whose financial needs are expected to change over time.

Young professionals, growing families, business owners and people with fluctuating incomes often appreciate the policy flexibility.

For example someone expecting career growth might initially choose lower premiums and later increase coverage as income rises.

Business owners might also benefit from coverage because business obligations can change over time.

People interested in both protection and cash value growth might find adjustable policies attractive.

However individuals seeking low-cost coverage might prefer term or whole life insurance instead.

Choosing the policy requires careful evaluation of long-term financial plans.

Is Adjustable Life Insurance Worth It?

Whether adjustable life insurance is worth it depends on financial needs and long-term goals.

For individuals who value flexibility and lifelong coverage the policy can provide financial advantages.

The ability to change premiums and death benefits makes the policy adaptable to life stages.

Cash value accumulation also adds a layer of financial security.

However adjustable life insurance also involves costs, complexity and investment uncertainty.

People who do not need features might find simpler insurance products more practical.

Before purchasing any permanent insurance policy consumers should carefully compare costs, benefits and risks.

Professional financial advice can also help determine whether adjustable life insurance fits financial situations.

Final Thoughts

Adjustable life insurance offers a combination of flexibility, permanent protection and cash value growth.

For people these features create valuable long-term financial security.

The ability to adjust premiums and death benefits allows policyholders to adapt their coverage as life circumstances change.

At the time adjustable policies come with higher costs and greater complexity than simpler insurance options.

Understanding both the benefits and risks is essential before making a decision.

For individuals seeking lifelong protection adjustable life insurance can be a powerful financial planning tool.

For others focused on affordability and simplicity term or whole life insurance might provide better value.

Carefully evaluating your income, family responsibilities, future goals and risk tolerance will help you decide whether adjustable life insurance is the choice for your financial future.

Frequently Asked Questions (FAQs)

What is adjustable life insurance?

Adjustable life insurance is a type of life insurance that allows policyholders to change certain parts of the policy over time.

These changes might include premium payments, death benefits or coverage terms depending on needs and the insurance companies rules.

Unlike policies with fixed structures adjustable life insurance offers flexibility as life situations change.

How does adjustable life insurance differ from life insurance?

The main difference between life vs adjustable insurance is flexibility.

Whole life insurance has fixed premiums and fixed death benefits while adjustable life insurance allows policyholders to modify coverage and premiums over time.

Whole life insurance is generally simpler and more predictable whereas adjustable life insurance offers customization options.

Does adjustable life insurance build cash value?

Yes adjustable life insurance includes a cash value component.

Part of the premium payment goes into a savings- account that grows over time on a tax-deferred basis.

The cash value can sometimes be borrowed against. Used for future financial needs such as retirement income, emergencies or education expenses.

Is life insurance more expensive than term insurance?

Yes adjustable life insurance is usually more expensive than term life insurance because it provides coverage and builds cash value.

The flexibility features and lifelong protection increase the policy cost compared to temporary term insurance policies.

Can I increase my death benefit later?

Yes many adjustable life insurance policies allow policyholders to increase their death benefit later if their financial responsibilities grow.

However the insurance company might require medical underwriting or health evaluations before approving higher coverage amounts.

What happens if I lower my premium payments?

Lowering premium payments might reduce the growth of the policies cash value. Affect the long-term stability of the policy.

If premiums become too low the policy might eventually lapse if there is not cash value to cover insurance costs and fees.

This is why it’s essential to monitor life insurance carefully.

Is life insurance a good investment?

Adjustable life insurance is mainly designed for financial protection rather than aggressive investment growth.

While the cash value component can grow over time returns might be lower than some investment options like stocks or mutual funds.

However many people value the policy stability, tax advantages and financial flexibility.

Who should consider life insurance?

People with changing financial responsibilities often benefit most from adjustable life insurance.

Young families, business owners, professionals with growing income and individuals interested in term financial planning might find the flexibility useful.

The policy can adapt to changing life stages easily than fixed insurance products.

Can adjustable life insurance expire?

Long as premiums are maintained and policy conditions are met adjustable life insurance provides lifelong coverage.

However poor policy management, insufficient premiums or low cash value growth could potentially cause the policy to lapse.

Regular reviews, with an advisor can help prevent coverage problems.

Is life insurance worth it?

Whether adjustable life insurance is worth it depends on financial goals, income stability and long-term needs.

For people seeking flexibility, permanent coverage and cash value growth it can provide benefits.

However those wanting affordable coverage might prefer term or whole life insurance instead.