Introduction

Term life insurance is considered one of the simplest and least expensive forms of coverage currently on the market. Unlike permanent policies, it offers coverage for a specific period, typically 6 to 12 months, depending on your needs. It is important to know the duration of your policy, whether you are securing your family’s future, covering a mortgage, or planning for your children’s education.

In this article, we will break down everything you need to know, starting with the basics and moving on to key insights to help you make a smart decision.

What is term life insurance, and how does it work?

Term life insurance is an agreement between you and an insurance company. In exchange, you will pay the insurer a fixed premium, and in the event of your passing within the period of the term, the insurer will pay your beneficiaries a death benefit. It is strictly protection-based; there is no investment element, so it is usually cheaper than permanent life insurance.

Some of the main characteristics of Term Life Insurance.

Fixed Term Duration

Its fixed-term period is the most distinguishing aspect. This implies that your policy will be limited to a certain number of years – usually 10, 20, or 30 years. At this time, your coverage is still in effect, provided you continue to pay premiums.

Level Premiums

In most policies, the premiums are level; that is, the amount you pay remains the same throughout the selected period. This predictability makes budgeting easier and helps you plan in the long term.

Death Benefit Protection

If the insured person covered by the policy passes away during the policy term, the policy will pay a lump-sum tax-free benefit to the beneficiaries. This money may be utilized in anything, either daily bills, debts, or financial requirements in the future.

Whole Life vs. Term Life Insurance.

One of the major differences to be aware of is between term life and whole life insurance.

Term Life Insurance: Temporary cover that has a specified term.

Whole Life Insurance: Lifetime cover that includes a savings feature.

Term life is usually the preferred choice if your primary interest is affordability and short-term financial security.

Understanding Policy Maturity

Policy maturity is another important concept. This is the time when your term life insurance policy is over at the expiry of its agreed period. There are a few things that may occur at this stage:

• The policy lapses without any payout (in case no claim was made)

You can also choose to renew the policy.

• You can possibly transform it into a permanent policy.

Policy maturity is something that you can understand, so that when the next step is to be taken, you can plan it well in advance.

How Long Is Term Life Insurance? Understanding Term Duration Options

The term life insurance does not have a set length of term; it depends on the length of term you select. Insurers are offering numerous options of term duration to enable you to match your insurance with your financial commitments.

Common Term Duration Options

10-Year Term

A short-term solution is best suited to individuals with temporary financial commitments. For example:

• Repaying a personal loan.

• Close a narrow income disparity.

This kind of term period is normally the cheapest yet with limited long-term coverage.

20-Year Term

A 20-year term is frequently chosen because a young family would want a 20-year term. It can cover:

• Children’s upbringing

• Mortgage payments

• Early career financial risks

30-Year Term

It is a longer-term period that offers longer-term peace of mind and is best suited to:

• Long-term financial planning

• Income replacement

• Paying off big debts such as home loans.

Even though the premiums are higher than those for short-term coverage, they will remain constant over a longer period.

Custom Term Options

There are insurers who have flexible periods, like:

• 5 years

• 15 years

• 25 years

These enable you to customize your policy to meet your specific requirements.

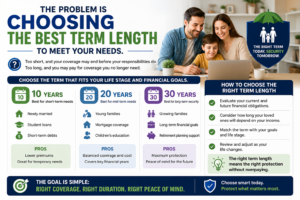

What Is the appropriate period of the term?

The duration of the right term should be chosen based on a number of individual factors:

Age

Younger people tend to choose a longer term because premiums are lower and responsibilities are only beginning to emerge.

Financial Responsibilities

Consider the time your dependents will be living off your income. For example:

• Until children graduate

• Until debts are paid off

Long-Term Goals

Adjust your coverage to major milestones such as retirement and significant investments.

Real-Life Examples

To get a better idea of the length of term life insurance, we would consider two easy cases:

Example 1: Young Parent ( Age 30 )

A 30-year-old with two young children may opt for a 20- or 30-year term to ensure they are financially covered until the kids grow up and become independent.

Example 2: Mid-Career Professional (Age 45)

A person nearing retirement may choose a 10- or 15-year term to cover outstanding debts and provide a financial cushion.

Why Term Duration Matters So Much

The duration of your policy is not merely a figure, but it has a direct influence on:

• Your premium costs

• Your family’s financial security

• How well your coverage works.

Selecting an incorrect term length may leave you either undercovered or still paying a premium you do not need.

Wrapping Up Part 1

Fact #1- Term Life Insurance Is Flexible in Its Term Duration.

Term life insurance is not a rigid financial product, as you can choose a term duration that best fits your life stage, financial goals, and responsibilities. This makes it a viable option for a diverse group of people, regardless of their age: a young professional, a family, and even someone approaching retirement.

Short vs. Long Term Duration.

Short-Term Duration (5–15 years)

This is perfect in cases when you have interim financial commitments like:

Examples of this include:

Covering a short-term business risk.

• Filling a gap prior to retirement.

Shorter policies tend to have lower premiums and are therefore affordable. Nevertheless, they might not provide sufficient cover to meet long-term requirements.

The increased term period is more appropriate when it comes to the larger life demands, like:

• Raising children

• The settlement of a mortgage.

• Income replacement assurance for your family.

Although the premiums are higher than those for short-term policies, they provide long-term financial security and stability.

Customization Based on Life Goals

• A 20-year plan for the education schedule of your child.

• 30-year policy on a newly bought house.

• A 10-year plan of outstanding debts at retirement.

It is this flexibility that makes it so important to know how long-term life insurance is- it is not just a matter of length, but of timing your coverage and getting it right.

Fact 2 – It is the Policy Maturity that determines what happens at the End.

What Is Policy Maturity?

So, what happens at Policy Maturity?

When your policy is mature, then you usually have a number of choices:

Policy Expiration

The easiest consequence is that the policy terminates, and coverage ceases. If no claim is made during the term, no payout is issued.

Policy Renewal

Most insurers will enable you to renew your policy once it has matured. However:

• Premiums will go up substantially.

• Pricing might be influenced by your age and health.

Renewal may also increase your term length; however, it will usually be more expensive.

Policy Conversion

Certain policies offer a conversion option that lets you convert to permanent life insurance without a medical exam. It may be a good alternative if your health changes.

Return of Premium Policies.

Some term policies have a return of premium feature. If you live beyond the term of office, the premiums you paid will be refunded. Although these policies are less costly, they offer an added level of financial security.

The importance of Policy Maturity.

It is important to understand policy maturity as it will enable you to:

- Planning your financial future.

- Keep coverage gaps to a minimum.

- Decision: To renew, convert, or terminate your policy.

You may also end up uninsured at a time when you still require insurance.

Fact #3- Riders are able to extend or improve their coverage.

What Are Riders?

The other benefits that you can add to your term life insurance policy to provide additional protection are the riders. They also enable you to tailor your coverage beyond the standard.

Riders of common types.

The following are some of the most popular riders that can be purchased:

- Accidental Death Rider

Gives an extra payout in case of death as a result of an accident. - Critical Illness Rider

Pays a lump sum in case you prove to be suffering from a serious illness like cancer or heart disease. - Waiver of Premium Rider.

In the event of disability or inability to work, this rider will not require you to pay premiums, and the policy will remain active. - Term Extension Rider

This is particularly applicable when the term duration is taken into consideration. It enables you to extend your cover under specific circumstances without taking out a new policy.

The Influence of Riders on the Duration of Term.

Although riders do not necessarily have a direct effect on the length of your policy, they can:

• Prolong benefits not just to the initial period of termination.

• Provide coverage in special situations

• Minimize risks in finances in the event of any unforeseen occurrences.

To illustrate, a waiver of premium rider is a feature that keeps your policy active until the desired term, even if you are unable to pay due to a disability. This is basically a waiver-of-premium rider, in which case you are unable to pay but want to keep your policy active until the desired term.

The Reason Riders are Worth Considering.

Riders will help strengthen and enhance the flexibility of your policy. You may not need to purchase several insurance products, but you can upgrade your current plan to better suit your changing needs.

However, it’s important to:

• Compare the price of each rider.

• Select only those that are in accordance with your financial requirements.

• Do not take any unnecessary add-ons that add value to premiums without actual value.

Wrapping Up Part 2

• Flexible coverage period gives you the opportunity to adjust your coverage according to your stage of life.

Policy maturity: What happens when your coverage expires?

• Riders complement and, occasionally to a greater extent, increase the value of your policy.

These are key determinants of the extent to which your term life insurance is useful.

The rest of the facts, such as renewal options, conversion strategies, and how to ensure that you save some money in the long run by simply picking the right term duration.

Fact #4 – You Can Add Renewal Options, Which Can Add to the term you already have.

What Is Policy Renewal?

Policy renewal is an opportunity to continue your term life insurance policy once it matures. This does not imply that you need to buy an absolutely new policy off the shelf.

How Renewal Works

• No medical examination is normally needed.

• You are recalculated on the basis of your present age with regard to premiums.

Although effective in extending your term, renewal comes at a price, that is, at a higher cost.

Cost Implications of Renewal

It can be much more costly to renew a policy since:

• You’re older

• The health risks could have been increased.

• The insurer is taking on a higher risk

This is why renewal is mostly viewed as a short-term project rather than a long-term plan.

When Renewal Makes Sense.

• You still have financial obligations

• Your well-being is compromised, and new policies are costly.

• You have a temporary need for insurance as you strategize on what to do next.

Knowing renewal options will help you better plan what to do after the policy matures and ensure you are not left without cover.

Fact #5 -Conversion options have an effect on policy maturity.

What Does Policy Conversion Entail?

Conversion is a feature that lets you convert your term life insurance into a permanent one (such as whole life insurance) without a medical exam.

Why Conversion Matters

The alternative will have a significant effect on your financial future, as it will alter the way policy maturity works.

• Term life insurance has a definite expiration.

Permanent insurance is a type of insurance that offers lifetime coverage.

By converting your policy, you are effectively lifting the restrictions on your policy’s initial term.

Benefits of Conversion

- Lifelong Coverage

Upon conversion, your policy does not expire upon policy maturity. - No Physician Exam.

Although your health might have deteriorated, you can still get long-term coverage. - Builds Cash Value

Permanent policies usually include a savings element that accumulates over the years.

When Do You Think It is Time to Convert?

A conversion is an intelligent alternative when:

• You would like lifetime protection.

• Your economic condition has become better.

• You have estate or legacy plans.

It is worth noting, though, that premiums in permanent insurance are higher, so budgeting is paramount.Fact #6- Selecting the Appropriate Term Duration Saves Money.

Comparison of Cost in the Short vs. Long Term.

Shorter period of termination. Reduced premiums and limited cover.

Longer term: The longer the term, the higher the premium, but the longer the protection.

The idea is to strike a balance between affordability and sufficient coverage.

There is a risk of making the wrong choice regarding the term duration.

Too Short:

• Coverage ceases prior to your financial commitments.

• You might have to renew at a significantly increased price.

Too Long:

• You are paying for coverage that you no longer require.

• Other investments could be made using money.

Meeting Life Goals with Term Duration.

To make the best decision, match your term duration with your major financial responsibilities:

• Mortgage → Select a term that corresponds to your loan term.

• Education of children -until they are independent.

• Income replacement → Credit to your working years

Savvy Money-Saving Strategies.

• Avoid overestimating your coverage needs

• Riders should be used wisely rather than purchasing a series of policies.

Making an informed decision regarding the term duration will help you maximize your policy.

The problem is choosing the best term length to meet your needs.

Step 1: Evaluate Your Financial Responsibilities.

• Loans and debts

• Family expenses

• Future education costs

Step 2: Approximate You Have Covered Timeline.

Step 3: Consider Your Dependents.

Step 4: Review Your Budget.

Step 5: Include Riders and Policy Maturity.

Plan in advance for the maturity of policy, so that one is not taken by surprise.

General Errors in Choosing a period of time for which the Life Insurance covering the long term should be.

- Selecting an Inadequately Short-Term Duration.

This may leave you without cover when you still need it. - Ignoring Policy Maturity

The consequences of failing to plan for the policy’s maturity can include a sudden lapse in coverage. - Overlooking Riders

Failing to consider riders will result in overlooking some of the best customization features. - Underestimating Future Needs

Life is changing fast–your insurance must be able to consider that.

Conclusion

Then, what is the length of term life insurance? The solution is tailored to your personal needs, financial objectives, and life stage.

In this guide, we have discussed six facts that are powerful and shape your decision:

• Term customization can be done by the flexibility of term duration.

Policy maturity dictates what happens at expiry.

• Riders enhance and extend coverage

Renewal options: You can extend your policy through renewal options.

Options to conversion may be lifetime-guaranteed.

• Selecting the appropriate term helps to save money.

The most important thing to remember is the following: do not base your policy choice solely on price. Rather, concentrate on how you can match your term duration, policy maturity planning, and how you use your riders in order to create a policy that truly helps you protect your future.