Is Life Insurance an Asset? 9 Strong Facts To Estate and Value.

Part 1: Introduction + Understanding Life Insurance + Is Life Insurance an Asset?

Introduction

One of the most significant financial instruments that is used by individuals and families in the United States is life insurance. It offers monetary security, stability among the loved ones, and, primarily, long-term financial planning. But one question that is very likely to cause confusion is: Is life insurance an asset?

This is not a simple answer as many people believe. Whereas these kinds of life insurance may be regarded as an asset, others cannot. This difference is very important to understand, particularly when it comes to estate planning, calculating your net worth, and managing financial resources effectively.

In the USA, Life Insurance policies are frequently used not only to provide protection but also to build wealth, plan taxes, and avoid legal hassles such as probate. Moreover, the policy value concept significantly affects whether a life insurance policy can be considered an asset.

In this guide, you will learn:

What life insurance is and how it works

Whether life insurance should be considered an asset.

The difference between term and permanent policies

Policy value and its impact on financial classification.

At the conclusion of this section, you will have a clear picture of the fundamentals before going into greater financial and legal understanding in the later sections.

What Is Life Insurance?

To answer whether life insurance is an asset, it is important to understand what it is and how it works.

Basic Definition

Life insurance is a contractual agreement between a person (policyholder) and an insurance firm. The insurer, in exchange, agrees to pay a sum of money, which is known as the death benefit, to persons designated to receive that benefit, in the event of the death of the policyholder.

This funding will be able to finance:

Funeral expenses

Outstanding debts

The living expenses of family members on a daily basis.

Education and other future financial requirements.Several varieties of Life Insurance.

The United States has two major types of life insurance:

Term Life Insurance

Term life insurance is a policy that covers a specific period, e.g., 10, 20, or 30 years.

Key features:

Lower premiums

No savings or investment component

Only paid out upon the death of the policyholder within the term.

Term life insurance is generally not considered an asset because it typically does not increase in value over time.

Permanent Life Insurance

Permanent life insurance comprises policies such as whole life and universal life. These policies offer lifelong cover and contain a savings aspect.

Key features:

Higher premiums

Lifelong protection

Grows policy value (cash value) with time.

It is this cash value that frequently makes permanent life insurance an asset.

Important Elements of a Life Insurance Policy.

In order to grasp the way life insurance works in detail, one will need to be aware of the key elements of this insurance:

Premium

The monthly payment you make to ensure that the policy is still in operation.

Death Benefit

The amount of money your beneficiaries will get when you die.

Cash Value (Policy Value)

A savings feature of permanent life insurance that accumulates over time and may be withdrawn during your lifetime.

Is Life insurance an asset?

Now we will consider the fundamental issue: Is life insurance an asset?

What Is an Asset?

An asset is anything of a financial nature and can be owned, controlled, or converted into cash. Examples include:

Real estate

Savings accounts

Investments

To be considered an asset, an asset must deliver quantifiable economic benefits.As an asset, Life Insurance is considered an Asset.

Life insurance may be viewed as an asset; however, it is provided only if certain conditions are met.

Permanent Life Insurance as an Asset.

Whole life or universal life insurance policies are among those whose value accumulates over time. This cash value:

Grows by paying premiums.

Can be borrowed against

Can be withdrawn under certain conditions

Since it can be identified and determined to have real, accessible financial value, it is regarded as a financial and estate planning asset.

Term Life Insurance is NOT an Asset.

Term life insurance is not value-accumulating. It is merely a death benefit provided if the policyholder dies during the period of coverage.

Since:

It does not have cash value.

It is not available during the lifetime.

Generally, it is not regarded as an asset.

Policy Value role in Asset Classification.

The most critical factor in determining whether life insurance is an asset is the policy’s value.

Why is Policy Value Important?

It is actual money that is owned by the policyholder.

It is accumulated with the passage of time by way of interest or dividends.

It can be used during the policyholder’s lifetime

Due to these characteristics, policies whose value is in cash are frequently part of:

Net worth calculations

Financial portfolios

Long-term investment strategies

Financial Planning in Life Insurance.

Permanent policies in modern Life Insurance in the USA are commonly incorporated into a broader financial plan.

They can:

Provide long-term savings

Support retirement planning

Assist in the efficient transfer of wealth.

Also, life insurance will be important for eliminating complexities such as probate, as beneficiaries will receive the money in hand quickly.

Conclusion of Part 1

In Part One, we have been able to present the fundamental basis upon which we should consider life insurance as a financial instrument:

What life insurance is and how it works

The difference between term and permanent policies

The meaning of an asset and its application to life insurance.

Why is policy value the most relevant in deciding asset status?

Is Life Insurance an Asset? 9 potent facts about estate and value.

Part 2: Policy Value, Estate Planning & 9 Powerful Facts.

Knowing Policy Value of Life Insurance.

In order to give a full answer to the question: Is life insurance an asset? You need to understand the term’ policy value’. This is what makes or breaks a life insurance policy: it determines whether there is financial value beyond the death benefit.

What Is Policy Value?

Policy value or cash value is a savings component in permanent life insurance policies, such as whole life or universal life.

Over time:

OB: A portion of your premium is spent on insurance.

Another part is invested / saved by the insurer.

This figure increases in cash.

It implies that your life insurance policy not only serves as protection but can also serve as a financial asset.

The Increasing Policy Value.

Policy value grows depending on the sort of policy you possess.

Whole life insurance: Grows at a fixed rate.

Universal life insurance: Growth will be based on interest rates or market performance.

Dividend-paying policies: Can be used to create value over time.

It is this gradual build-up that renders permanent life insurance an appealing investment in a long-term financial plan.

How Policy Value can be used by you.

The greatest benefit of the possession of policy value is that you can avail yourself of it when you are still alive.

You can:

Take loans against the policy

Withdraw funds

Use it as collateral

It is this flexibility that has led many financial planners to view permanent life insurance as part of a broader estate planning strategy.

Policy Value vs Death Benefit.

It is necessary to know the difference:

Policy Value → Money that you may draw upon during your lifetime.

Death Benefit → Money given to the beneficiaries upon death.

Although the value of both is substantial, only the one in the form of a policy has a direct impact on your personal financial resources throughout your lifetime.

The use of Life Insurance in Estate Planning.

The significance of life insurance in estate planning is particularly pronounced in the United States, where wealth transfers must be efficiently managed.

Reasons why Life Insurance is important in Estate Planning.

Life insurance is used to secure your loved ones with money in case of your death. This can offer instant cash when it is most needed.

It is often used to:

Replace lost income

Pay off debts

Cover funeral expenses

Support dependents

Avoiding Probate

Among the greatest benefits of life insurance is its ability to avoid probate.

What Is Probate?

Probate is a legal procedure of allocating the assets of a deceased person via the court system. It can be:

Time-consuming

Expensive

Public

The benefits of Life Insurance.

Upon naming a beneficiary:

The payout goes directly to them

It does not go through probate

Money is raised more quickly.

This renders life insurance a potent device in streamlining the allocation of the estate.

Providing Estate Liquidity

When an individual dies, he or she may have an estate comprising property or investments that are difficult to convert into cash.

Life insurance provides:

Immediate liquidity

Money to pay taxes or debts.

tability in the transitions of finances.

Wealth Transfer Strategy

Life insurance is a common way to transfer wealth effectively between generations.

Benefits include:

Fast flow of finances.

Reduced legal complications

Potential tax advantages

This makes it a major part of contemporary financial planning for Life Insurance in the USA.

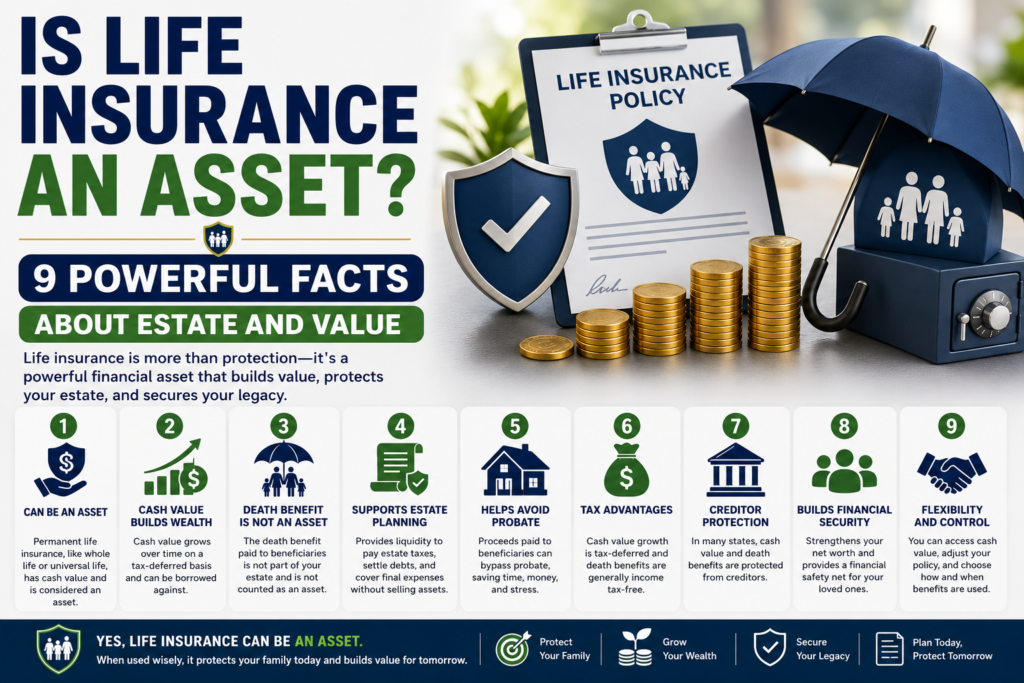

9 Life insurance as an asset: powerful facts.

Having discovered the value of policy and estate learning, it is now time to identify the key factors that determine whether life insurance is truly an asset.

Fact #1: Not Every Life Insurance Policy is an Asset.

The greatest myth is that not every life insurance policy is an asset.

Term life insurance → Not an asset.

Permanent life insurance (Permanent) → Can be an asset.

Policies that have policy value are only eligible.

Fact #2: Cash Value Policies Build Wealth Over Time

Permanent life insurance policies have a cash value that grows consistently.

This means:

The value of your policy increases with time.

It can be included in your financial portfolio

It helps in long-term prosperity.

Fact 3: It is possible to borrow Policy Value.

A special benefit is that you can borrow on your policy.

This allows you to:

Access funds do not sell assets.

Maintain financial flexibility

Apply the policy as a backup in the form of a monetary allowance.

Fact #4: Life Insurance Can Avoid Probate.

As mentioned above, life insurance is usually exempt from probate.

This means:

Faster payouts

Less legal hassle

Greater privacy

This is the only feature that renders it very important in estate planning.

Fact #5: It is an important aspect of Estate Planning.

Life insurance is not merely insurance but a financial instrument.

It helps:

Protect wealth

Ensure the transfer of assets is smooth.

Promote long-term planning objectives.

Fact #6: Designation Beneficiary Designation Is More Important Than Ownership.

Most of the time, the beneficiary named decides who will receive the funds, not the policy owner’s will.

This brings to the fore the significance of:

Maintaining the beneficiary information.

Setting it along with your estate planning objectives.

Fact #7: Life Insurance could have Tax Benefits.

In most cases:

Death benefits are tax-free.

Ober Policy value increases tax deferred.

This renders life insurance an effective financial tool.

Fact #8: It Makes Instant Liquidity.

Life insurance is unlike real estate or investments, as the money is received instantly upon death.

This is essential to:

Paying debts

Covering expenses

Supporting family members

Fact #9: Policy Value May be included in your Net Worth.

If your policy has cash value, it can be added to your total net worth.

This particularly applies to:

Financial planning

Retirement strategies

Wealth management

Conclusion of Part 2

In this part, we looked into the more financial and strategic nature of life insurance:

Working and the importance of policy value.

Why life insurance is important in estate planning.

How it helps avoid probate and provides liquidity

The 9 key facts that make life insurance an asset.

Is Life Insurance an Asset? 9 Facts of Power about Estate and Value.

Part 3: Legal Concerns, Advantages and Disadvantages, Myths, Frequently Asked Questions, and Final Reflections.

Probate and Life Insurance explained.

To gain a complete picture of whether life insurance is an asset, it is important to consider how it interacts with probate, a major aspect of estate planning.

What Is Probate?

Probate is the legal procedure by which the assets of the deceased person are distributed under court supervision. This is done to make sure that the debts are paid and the rest are transferred to the heirs.

However, probate can be:

Time-consuming (usually months or years)

Expensive because of legal expenses.

Public, that is, financial information can become available.

How Life Insurance Avoids Probate

The fact that it typically avoids probate altogether is one of the greatest benefits of life insurance in the United States.

In case of a valid beneficiary, named:

The death benefit is paid off-hand by the insurance company.

The money is directly deposited into the recipient’s account.

There is no court involvement.

This renders life insurance a potent instrument in effective estate planning.

The Rule has exceptions.

In some cases, life insurance can be subject to probate:

If it is the estate that is referred to as a beneficiary.

then, in case of the absence of beneficiaries.

In case all the beneficiaries are deceased.

In such instances, the payout will be part of the estate and may be subject to probate delays.

Legal and Financial factors.

When deciding whether life insurance should be considered an asset, it is necessary to understand its legal and financial aspects.

Ownership vs Beneficiary

Among the major differences in life insurance in the USA is the distinction between policy ownership and beneficiary designation.

Policy Owner: Controls the policy and can make changes to it.

oveneficiary -> is given the payout upon death.

This difference matters because ownership influences control, whereas the beneficiaries decide who gets the money.

Tax Implications

There are various tax benefits of life insurance, though there are exceptions.

Tax Benefits

Death benefits: In general, death benefits are tax-free.

The value of the policy increases tax-deferred.

Potential Tax Issues

Estate taxes can only apply to large estates.

In some cases, withdrawals of cash value are subject to taxation.

The right planning will guarantee the maximum benefits at minimum tax effects.

State legislation and differences.

Life insurance legislation in the USA may vary by state. These variations can impact:

Beneficiary rights

Tax treatment

Estate inclusion

It is always prudent to seek the advice of a financial consultant or other legal expert when integrating life insurance into your financial plan.

The merits and demerits of Life Insurance as a Resource.

Like any other financial instrument, life insurance has both advantages and drawbacks as an asset.

Advantages

1. Financial Security

Gives strength and care to loved ones.

2. Tax Benefits

Provides tax-free death benefits and tax-deferred growth.

3. Liquidity

Gives instant cash when required.

4. Wealth Transfer

Helps efficiently pass assets to beneficiaries without probate.

Disadvantages

1. Premium Costs

Permanent life insurance can be expensive.

2. Small Liquidity (Term Policies)

A term life policy does not accumulate a policy value and thus cannot be drawn in the form of cash.

3. Complexity

It can be complicated to understand the terms of policies, taxes, and legal regulations.

There are certain myths about life insurance.

Many people misconstrue the concept of life insurance operations, particularly regarding assets.

Misconception #1: All Life Insurance Is an Asset

Reality: Only policies with policy value (cash value) are considered assets.

Misconception #2: Life Insurance never pays any taxes.

Reality: Although death benefits are typically not subject to tax, they may still suffer estate taxes or withdrawals.

Misconception #3: Life Insurance Is Only Useful after Death.

Reality: Permanent policies enable you to access cash value in your lifetime.

Misconception #4: Beneficiaries are never final.

Reality: Beneficiaries can be changed, and a conflict may arise due to documentation ambiguity.

Frequently Asked Questions about Life Insurance as an Asset.

Q1: Does the USA regard life insurance as an asset?

Yes, but permanent life insurance policies are considered assets only if they have a policy value. Term life insurance is not usually considered an asset.

Q2: Does life insurance go through probate?

No, life insurance does not normally go to probate if a beneficiary is named. But it can be subject to probate, provided that the listing shows the estate as beneficiary.

Q3: Is it possible to use policy value during life?

Yes, you may borrow against the policy’s cash value of a permanent life insurance policy.

Q4: How does life insurance help in estate planning?

Life insurance is liquid, eliminates probate, and helps transfer wealth efficiently, making it an important component of estate planning.

Final Conclusion

Therefore, is life insurance an asset? This is determined by what kind of policy you have.

Term life insurance → Not an asset.

Permanent life insurance → Can be a valuable asset due to its policy value

The current Life Insurance in the USA is no longer focused on protection but is a potent financial instrument used in estate planning, wealth transfer, and long-term financial planning.