Challenging Beneficiary of Life Insurance: 8 Legal Facts that are Powerful.

Part 1: Introduction + Understanding Beneficiaries + Meaning of Contesting.

Introduction

Life insurance is meant to give the loved ones financial security and peace of mind in the event of the death of a person. The United States has millions of families that use policies as a safety net to meet the costs, debts, and future needs. But even with the intent, the cause of disagreement over who gets the payout is more common than people might imagine.

Contesting life insurance beneficiary designations is one of the most complex issues in life insurance in the USA.

As soon as disagreements arise, whether due to family conflict, a sudden change in policy, or legal issues, these cases may quickly become serious legal matters.

It is crucial to understand how beneficiary designations work and when they may be contested by anyone involved in a life insurance policy. There are other situations in which the ultimate recipient of benefits may be influenced by factors such as insurable interest, fraud, or even Medicaid claims.

In this guide, you will learn:

What is a life insurance beneficiary and how s/he is selected?

What it entails to challenge a beneficiary.

• Typical causes of conflicts.

• Legal terms that are important in informing such cases.

At the conclusion of this section, you will have a sound basis upon which to establish the nature of how these disputes operate before getting into the legal facts and processes in subsequent sections.

Learning Life Insurance Beneficiaries.

It is worthwhile to comprehend the role of a beneficiary in a life insurance policy before discussing disputes.

What is a Beneficiary?

One beneficiary is the individual (or organization) who receives the life insurance payout upon the policyholder’s death. It is sometimes referred to as the death benefit, a payout usually paid directly to the beneficiary without probate.

Beneficiaries can include:

Family members (spouse, children)

• Friends or partners

• Trusts or organizations

This benefit grants the policyholder the legal right to decide who receives it, making the designation a powerful financial choice.

Types of Beneficiaries

Policies of life insurance generally contain two primary kinds of beneficiaries:

Primary Beneficiary

This will be the first in line to receive the payout. When the main beneficiary is alive at the policyholder’s death, he/she will receive the full benefit.

Contingent Beneficiary

This individual also receives the payout when the primary beneficiary is unable or unavailable to receive it.

The two types provide the insurance policyholder with a guarantee that his or her intentions will be adhered to even in unforeseen situations.

The manner in which the beneficiaries are selected.

In Life Insurance in the USA, the policyholder is at liberty to name or replace beneficiaries. This is normally done at any time by revising the policy documents.

Nevertheless, some legal regulations might be applicable:

• The policyholder should be mentally fit.

Any change has to be made in due process.

Some states (such as community property states) allow a spouse to have rights.

Since such a decision is legally binding, mistakes or dubious amendments can lead to future disputes.

Beneficiary Rights in the USA.

In most cases, the named beneficiary would have a clear legal right to receive the payout upon the policyholder’s death. The insurance companies must adhere to the terms of the policy unless there is a valid reason not to.

Nevertheless, these rights may be questioned in court in the case of evidence of:

• Fraud

• Undue influence

• Lack of insurable interest

• Other legal concerns

This is where conflicts start to emerge.

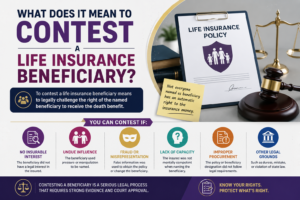

What Does it Mean to Contest a Life Insurance Beneficiary?

Now that we know what a beneficiary is, we should see what it is like to contest that label.

Definition of Challenging a Beneficiary.

Challenging the beneficiary of a life insurance policy is a legal challenge to the validity of the named beneficiary on a policy. This generally occurs when one feels that the designation is wrong, unjust, or illegal (unlawful).

Contesting is aimed at achieving:

• Switch the recipient of the payout.

• Block payment to the existing beneficiary.

• Settle disputes involving justifiable ownership.

Such cases are often subject to legal proceedings and may require court proceedings, lawyers, and thorough evidence.

When Do Disputes normally occur?

There are numerous situations when disputes over life insurance beneficiaries may occur, which include:

-

Family Conflicts

One of the most common reasons for legal conflicts is disagreement among spouses, children, or relatives.

-

Last-Minute Changes

When a policyholder changes his or her beneficiary just before death, this may signal that a wrongful act has been committed.

-

Suspicious Circumstances

- Issues could arise due to concerns over fraud, coercion, or manipulation.

-

Relationship or Divorce.

In other scenarios, former spouses can still be listed as beneficiaries, and after death, disputes can arise.

The reason why challenging a beneficiary is complicated.

It is not easy to contest a beneficiary of a life insurance policy. The policyholder usually prevails in court, and therefore, convincing a court that a designation ought to be revoked is a difficult legal task. Lexity in these cases is caused by factors such as:

• Strict legal requirements

• Need for clear evidence

• State-specific laws

• Participation of insurance companies.

Also, issues such as Medicaid claims or insurable interest may complicate the situation. Important Legal Concepts introduced.

At this point, you should be familiar with a handful of important terms that will be dealt with later in subsequent sections:

Insurable Interest: A legal prerequisite that guarantees that the beneficiary has a valid interest in the life of the policyholder.

Practicing Law: Medicaid Claims – Government claims that can influence the distribution of assets at the time of death.

• Legal Disputes- Disputes that need court intervention.

These concepts will give you a better understanding of the legal considerations of the dispute between beneficiaries.

Conclusion of Part 1

This first section has established a firm base, having discussed:

Role and significance of beneficiaries in Life Insurance in the USA.

How the beneficiaries will be selected and their legal rights.

• What it is to begin challenging claims to life insurance benefits.

• Why disputes can be complex and the common reasons why disputes arise.

On the basis of these fundamentals, one can delve deeper into the legal aspects of beneficiary disputes.

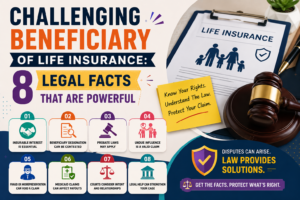

Contesting Life Insurance Beneficiary: 8 Powerful Legal Facts

Lawful Reasons to challenge the life insurance beneficiary.

No onNo one can succeed in challenging any policy without valid legal grounds. In the United States, courts do not reverse the beneficiary designations without a serious reason. The wishes of the policyholder are usually honored, except in the face of strong evidence to the contrary. The legal principles are critical to comprehend when challenging claims by beneficiaries of life insurance.

Absence of an Insurable Interest.

Insurable interest is one of the most crucial legal concepts in Life Insurance in the USA.

What Is Insurable Interest?

The tThe term insurable interest implies that the beneficiary of the policy has a valid financial or emotional stake in the policyholder’s life. Put differently, the beneficiary is expected to incur any loss in the event of the insured person’s death. Please include:

• Spouses

• Children

• Business partners

The reason It Matters in court cases.

Where the beneficiary lacks insurable interest, the policy may be invalid. Such arrangements can be perceived by the courts as unethical or even fraudulent.

It is frequently a key issue in significant judicial conflicts over life insurance payments.

Undue Influence

In undue influence, a person coerces or manipulates a policyholder into altering the beneficiary.

Typical indicators of undue influence.

• Beneficiaries’ sudden changes.

• Isolation of the policy owner.

• Reliance on a particular person.

Legal Impact

When established, courts can void the change of beneficiary and revert to an earlier beneficiary designation.

Fraud or Forgery

Another significant cause of challenging a beneficiary is fraud.

Examples of Fraud

• False signatures on policy documents.

• False data to make changes.

• Unauthorized alterations

Why It Matters

Fraud is taken seriously by insurance companies and the courts. In the event of fraud being established, policy payouts may be rerouted or delayed substantially.

Mental Incapacity

For a beneficiary change to be valid, the policyholder must be of sound mind when making the decision. Conditions that cause concerns.

• Dementia or Alzheimer’s disease

• Critical disease that impairs judgment.

• Medication influencing decision-making

Legal Consequences

If the policyholder was not in his right state of mind, the change may be invalidated.

divorce or family changes.

Families tend to be confused and to fight as a result of a family change.

Common Issues

Ex-spouses, who are still listed as beneficiaries.

• New partners who have not been informed of the policy.

• Children-children and spouses-spouses conflicts.

Legal Importance

Some states automatically revoke ex-spouses’ beneficiary status after divorce, whereas others do not, leading to complex legal battles.8 Strong Legal Facts on Challenging the Beneficiary of a Life Insurance.

Having known what the legal grounds are, we now move on to the most significant facts that can affect your case.

Fact 1: Beneficiary Designation Generally Takes Precedence over a Will.

Most individuals believe that the beneficiaries of their estates are decided by their will. Life insurance, however, operates differently. Key Point

The named beneficiary of a policy usually prevails over the direction in a will.

Why This Matters

An insurance company will typically pay the listed beneficiary unless the designation is successfully appealed.

Fact 2: Insurable Interest is a Legal Precondition.

As exAs explained above, insurable interest is also a critical factor in determining whether the policy is valid. Key Point

The pThe policy can be called into question or nullified if there is no insurable interest. Impact on Cases

This can be among the most effective arguments to present when challenging life insurance beneficiaries’ claims.

Fact #3: It has to be done fast when contesting.

In such cases, timing is very critical.

Key Point

Strict deadlines (statutes of limitations) exist for a claim.

Why It Matters

Inaction can lead to the loss of your right to contest the beneficiary, even in the case of a valid claim.

Fact #4: Evidence Is Critical.

Evidence plays a critical role in resolving disputes in court.

Types of Evidence

• Medical records

• Witness statements

• Policy documents

• Communication records

Key Insight

It is extremely hard to win a case without solid evidence.

Fact #5: Payouts can be impacted by Medicaid Claims.

In some cases, life insurance payouts will be complicated by the need to settle Medicaid claims.

How It Works

If the deceased was receiving Medicaid benefits, the government can seek to recover the expenses from the deceased’s estate.

Impact on Beneficiaries

Some of the payouts can be cut.

• Claims may delay distribution

• Legal issues can be encountered.

Knowing how medicaid claims relate to life insurance is crucial in complex situations.

Fact # 6: There is an automatic change in beneficiaries due to divorce.

In otIn other states, divorce laws affect beneficiary designations. Key Point

Under state law, an ex-spouse can be automatically disqualified as a beneficiary.

Why It Matters

Unless the policy is updated, this may cause confusion and legal issues over who is entitled to the payout.

Fact 7: Courts are conscious of the intent of policyholders.

The cThe courts seek to respect the policyholder’s true intentions. Key Point

In caIn cases of evident intent, the courts can adjudicate accordingly, even in tricky cases. Examples

• Written statements

• Witness testimony

• Consistent financial decisions

Fact #8: Payments may be slowed down by legal disputes.

Among the most feasible facts is the fact that conflicts are time-consuming.

Key Point

In contested cases, insurance companies tend to withhold payment until the matter is resolved.

Impact

• Beneficiaries may have to wait months or years.

• Legal fees may increase

• Emotional stress can grow

Conclusion of Part 2

In this section, we have discussed the legal basis of challenging life insurance beneficiary cases:

The most important legal bases are fraud, undue influence, and absence of insurable interest.

The 8 powerful legal facts that determine the outcomes in Life Insurance in the USA.

• The importance of medicaid claims and the ways that they can impact payouts.

• The reasons as to why sound evidence and prompt action are critical.

These insights highlight how complex and serious these cases can be.

Contesting Life Insurance Beneficiary: 8 Powerful Legal Facts

Part 3: Legal Process, Medicaid Claims, Risks, FAQs & Final Advice.

Five-step Guide to challenging a life insurance payout.

If you believe a beneficiary designation is invalid, it’s important to follow a structured legal process. To successfully challenge the claims of beneficiaries of life insurance, one needs to plan, document, and act accordingly.

Step 1: Review Life Insurance Policy.

The first step would be to acquire and thoroughly examine the policy inspections.

Look for:

• Current beneficiary designation

Date of last update

Policy terms and conditions.

This will help you determine whether there are any apparent problems or discrepancies.

Step 2: Determine Legal Justifications.

Then determine whether you have a sound legal basis to challenge the beneficiary.

Common grounds include:

• Lack of insurable interest

• Fraud or forgery

• Undue influence

• Mental incapacity

Your claim will not stand much chance without a sound legal foundation.

Step 3: Gather Evidence

Any successful case is based on evidence.

You may need:

Medical records (when claiming mental capacity)

• Witness statements

• Written or emails.

• Legal documents

The more evidence you have, the more chances you have of winning the dispute.

Step 4: Call the Insurance Company.

Inform the insurance company of the conflict as soon as possible.

In many cases:

• The payout can be temporarily retained by the insurer.

• An inquiry can be commenced.

• Further documentation can be ordered.

Quick communication can prevent funds from being released too early.

Step 5: Fill a Legal Claim.

In case the problem is not solvable directly, you might have to sue.

This typically involves:

• Hiring an attorney

• Making a claim in a court.

• Presenting your evidence

Since court cases may be complicated, it is strongly advised that one seek the assistance of a professional lawyer.

Medicaid Claims Role in Life Insurance.

Knowledge of medicaid claims is very crucial when handling life insurance claims, particularly in the United States.

What Are Medicaid Claims?

Medicaid is a government program that helps eligible individuals cover medical costs. Once someone dies, the government might seek to recoup some of these expenditures from their estate. The impact of Medicaid on life insurance.

In many cases:

• Life insurance proceeds are paid directly to beneficiaries.

The funds could not be considered part of the estate.

But there are problems that emerge when:

The beneficiary is the name of the estate.

Policy: Policies are designed in such a manner that they incorporate estate recovery.

Why is this important in Controversies?

In case of medicaid claims:

• Payments can be postponed.

• There might be a decrease in funds.

• Some further legal procedures might be needed.

This further complicates already complicated cases.

The Explained in Practice Insurable Interest.

Even though we mentioned insurable interest above, it is necessary to explain how it works in real-life situations. What is Insurable Interest?

There is a valid insurable interest where:

• A spouse relies either financially or emotionally on the policyholder.

• A business partner would suffer financial loss

• A family member is dependent on the insured.

What Does NOT Qualify?

• No relation to strangers.

Individuals are speculatively interested only.

• Cases that are planned to make some money with no harm.

Relevance in Court Cases.

If a court finds there is no insurable interest, the policy can be contested or canceled. This is a common point of contention in court in life insurance cases.

Ordinary Lawsuits that arise in Life Insurance claims.

Controversies about life insurance are common. Learning these situations would enable you to be aware of the risks involved.

Family Conflicts

Among the most prevalent factors that contribute to conflicts, disagreements between spouses, children, or relatives can be mentioned.

Fraud Allegations

Suggestions of forged documents or false information may result in severe legal problems.

Policy Ownership Issues

Misunderstandings about who owns the policy and who is the beneficiary may cause confusion.Last-Minute Changes

Alterations that occur just before one dies are mostly suspicious and subject to prosecution.

The importance of these disagreements.

All these situations may lead to protracted litigation, missed payments, and general stress for all the parties involved.

Dangers and Problems of Challenging a Beneficiary.

Although one can appeal against a beneficiary, one should be aware of the risks involved.

Legal Costs

It might be costly to hire an attorney and appear before the court, particularly when a case is lengthy.

Emotional Stress

Family members are often involved in disputes, making the process emotionally challenging.

Time Delays

It may take months or even years to solve cases, and access to funds may be delayed.

Uncertain Outcomes

Despite the strong evidence, no one knows whether they will be successful. The original designation may still be maintained by the courts.

Frequently asked questions concerning challenging the beneficiaries of a life insurance policy.

Q1: Is it possible to dispute a life insurance beneficiary?

Yes, Yes, a beneficiary may be contested for relevant legal reasons, including but not limited to fraud, undue influence, or lack of insurable interest.

Q2: What is the average duration of a dispute?

Depending on the complexity of the case and the degree of legal disputes a case involves, it may take several months to years.

Q3: What would it take to challenge a beneficiary?

The sources of evidence could include medical records, legal records, testimonies, and communication records.

Q4: Is there any relation between Medicaid claims and life insurance payouts?

Yes, under some circumstances, Medicaid claims may affect payouts, particularly when the estate is at stake.

Final Conclusion

Appealing a beneficiary’s life insurance claim is a complicated and sometimes difficult task. Although life insurance plans are supposed to bring sanity and financial stability, they can create conflicts due to legal, emotional, and financial issues.

By understanding:

• The legal process

Role of insurable interest.

• Effects of medicaid claims.

• Typical reasons for court cases.

They will help you navigate these situations more effectively and make informed decisions.

If you are considering contesting life insurance beneficiary claims, it is crucial to:

• Act quickly

• Gather strong evidence

• Get legal advice on a professional level.

And finally, the best weapon you have for effectively resolving these disputes is knowledge and preparation.